First things first. See disclaimer. Omada Health is a recent IPO. The S1 includes their unaudited financials going back to FY22. Omada IPO’d on June 9th of 2025. The company has never made a profit. They are currently free cash flow negative. I would caution all of you to do your own independent work, this is speculative with large customer concentration. I do not currently own shares, but I am watching them. I have concerns with their reliance on a single large customer that has had a large increase to A/R year over year.

Ticker: OMDA

Price: $16.29

Diluted Shares: 57,908,047 (as of last quarter)

Market Cap: $943 million

Cash: $198 million

Debt: None.

Enterprise Value: $744 million

What is it?

Omada Health is what’s known as a point solution. It’s a targeted solution for specific medical issues that operates as another layer of a healthcare plan or policy. Point solutions are typically carrier agnostic, meaning members of different health plans can still access the point solution if it’s being offered by their plan sponsor. Certain point solutions may even be integrated at the health plan level. There are plenty of point solutions available across the United States: Hinge Health, Livongo, Omada, Progyny, etc.

I should mention that the term “point solution” tends to imply a narrow focus on a specific offering. Omada has a few focuses: musculoskeletal (MSK), hypertension, diabetes, and obesity. Omada’s goal is to be a virtual-first care provider and to try and effectively “bend the cost curve.” What does that mean? If you can successfully intervene on a member of a health plan and get them treatment they abide by, and thus improve clinically, the cost of that member to the plan will go down along with the added bonus that the member is now healthier and happier. In short, if claims are down materially after intervention, your renewal may be more favorable as less claims have been paid and chronic conditions that the underwriter was previously concerned about abate.

History

Omada Health was founded by Sean Duffy in San Francisco in 2011. They raised private capital along the way from USVP, A16Z, Kaiser Permanente Ventures, Sanofi, Cigna Ventures, and dRx Capital (backed by Novartis and Qualcomm) amongst others. Omada raised a reported $450 million prior to the IPO to fund operations and grow. The valuation was north of $1 billion in the last round ($192 million Series E).

Omada Health IPO’d in June of 2025, the offered 7.9 million shares at $19.00/sh raising $150 million. The shares on IPO day rose double digits with a subsequent decline and then rose over the summer and into October. Since then, Omada has been in a nearly 40% draw down.

Care Model

The model that Omada puts forward is virtual first with human led care teams. Each member has access to licensed specialists that can assist them with their specific course of care.

In the diabetes and hypertension service, members are provided with a kit that includes glucose monitors, blood pressure cuffs, and smart scales. This hardware allows for automatic tracking of their relevant biomarkers, no manual logging is required. A key and important part of any point solution is member education and engagement, taking the burden off of the member and making it automatic is good for protocol adherence. Members also receive a care team that has access to their data, allowing the member to have tailored plans relevant to their specific needs.

In the GLP-1 Support service Omada is actually able to prescribe GLP-1s directly in all 50 states via their licensed provider network. The service includes nutritional guidance, behavioral coaching, and exercise specialists. All virtually. The focus is on keeping the weight off and 2/3 of Omada members that utilize GLP-1 Support maintained or kept losing weight after medication cessation. There is a unique angle to this GLP-1 Support that feeds into their other segment, MSK. GLP-1’s can cause rapid reduction in weight, but also muscle loss. In that event, they can integrate with their MSK Care segment.

The MSK Care segment is coined as a “virtual physical therapy clinic.” Licensed providers will virtually interact with their clientele to help diagnose their MSK issue. MSK is a major point of concern when it comes to health care claims (as is obesity, hypertension, and diabetes). I wrote a post about how high-cost claimants here:

High Cost Claimants Conditions

This piece will cover a variety of topics: Gene Therapies, Immunotherapies, High-Cost Claimants (referred to as: HCCs), general HCC Conditions. I will be inserting a small segment about medical billing codes as well. In a recent piece titled “Medical Stop Loss Dynamics” I discussed the concept of trend, leveraged trend, and lasers. These concepts are important as gene therapies can be expensive, but so can untreated individuals with ailments that can be improved/cured by these therapies. The piece can be read here (no paywall):

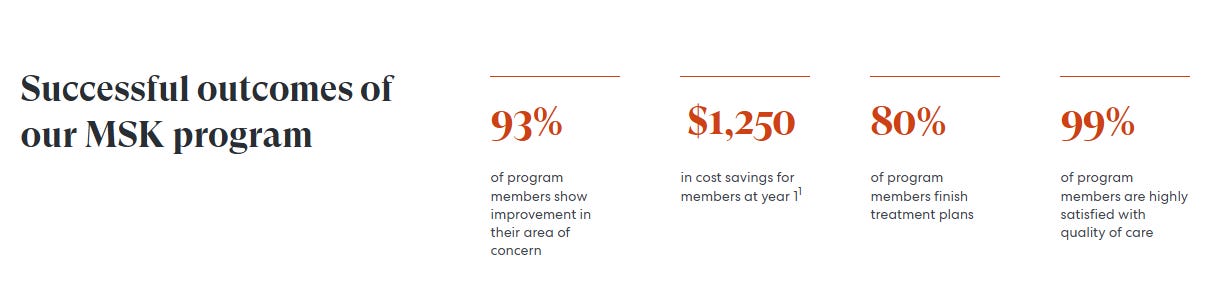

In that post I highlighted that for a specific Stop Loss carrier, MSK reimbursements totaled $476M in their block of business alone from 2021-2024. If you think across the entirety of the United States both self-funded, fully insured, level funded, ACA, Medicare, Medicaid, etc. you can get a sense of how expensive MSK is for our healthcare system and to the employer sponsored plans or insurance carriers that may hire Omada or even Hinge Health as a service. The MSK Care team is able to advise on PT routines, integrate with primary care and specialty care, and track progress. Omada estimates that there is a $14,000 average savings per case if you appropriately treat back pain with surgery (sometimes this is not feasible). Below is from their site:

Product Distribution

Product distribution occurs in a few ways, namely brokerage channels such as Mercer, Aon, Gallagher, Brown & Brown, etc. This channel grants them access to employer sponsored plan clientele. These plans are either traditional integrated, fully insured arrangements or self-funded. Omada utilizes the brokerage partners as a distribution channel to these buyers. Omada can also go directly to the clients, but a distribution channel like a broker is far easier given the scale of clients in each brokerage house. Another means of distributions is through true channel partner relationships. This arrangement is with health plans, PBMs, or other resellers directly.

The contractual distribution channel arrangement with health plans, PBMs, or resellers is extremely important to Omada. Specifically, due to the commercial arrangement that it has with Cigna. Cigna owns more than 5% of the shares outstanding through their venture arm. Omada has agreements with Cigna and their affiliate Evernorth.

The program with Cigna started as a pilot program where Cigna, following their investment, introduced Omada’s prediabetes solution to Cigna ASO clients. The program was a resounding success and the program was expanded into a strategic partnership. During that pilot, participants sustained weight loss of 3.5% to 5% of their body weight beyond one year, improved claims costs resulted in $424 to $972 in net medical cost savings over two years compared to non-participants (an ROI of 1.5x to 2x for employers), and 83% of the participants would recommend the program. The partnership now has evolved into a full Diabetes Prevention Program with expanded savings and bodyweight reductions vs the original pilot program. The partnership also includes Omada’s hypertension, GLP-1, and MSK programs as well. They were named the preferred providers for Evernorth’s “Digital Health Formulary.” Evernorth launched EncircleRx, a “cardiodiabesity” program for monitoring obesity, diabetes, and cardiovascular disease with Omada as the key partner. This program was also a success, with a reported 4.8% decrease in BMI in six months for the participants.

So, what’s the rub? Well, there certainly is one and it’s not immaterial, at least in my view. There’s customer concentration that comes along with distribution channels such as Cigna. In the 9 months ended 2025, Cigna affiliates represented 31 and 32% of the revenue, yes separately, meaning total exposure to Cigna is 63% of revenues. Accounts receivable between the two affiliates counted for 70%.

For that reason alone, I am staying clear for now and keeping it on a watchlist. What I would ideally see, is A/R flat, and customer concentration being reduced as the firm builds brand awareness amongst the brokers and integrates into other smaller health plans nationally.

There’s a few ways to read this in my opinion.

Partner B is having such success with the offering that their share of consolidated revenues has increased from 18% to 32% and because of the volume increase their A/R has increase in a proportional way.

Sales are increasing, but cash conversion is weak. If cash conversion is weak, FCF is hindered.

In fact, this can be seen, even without accounting for SBC their FCF is negative, with SBC being accounted for it’s even lower. Their change in cash during the Q3 period is a result of their IPO proceeds.

Financials & Results

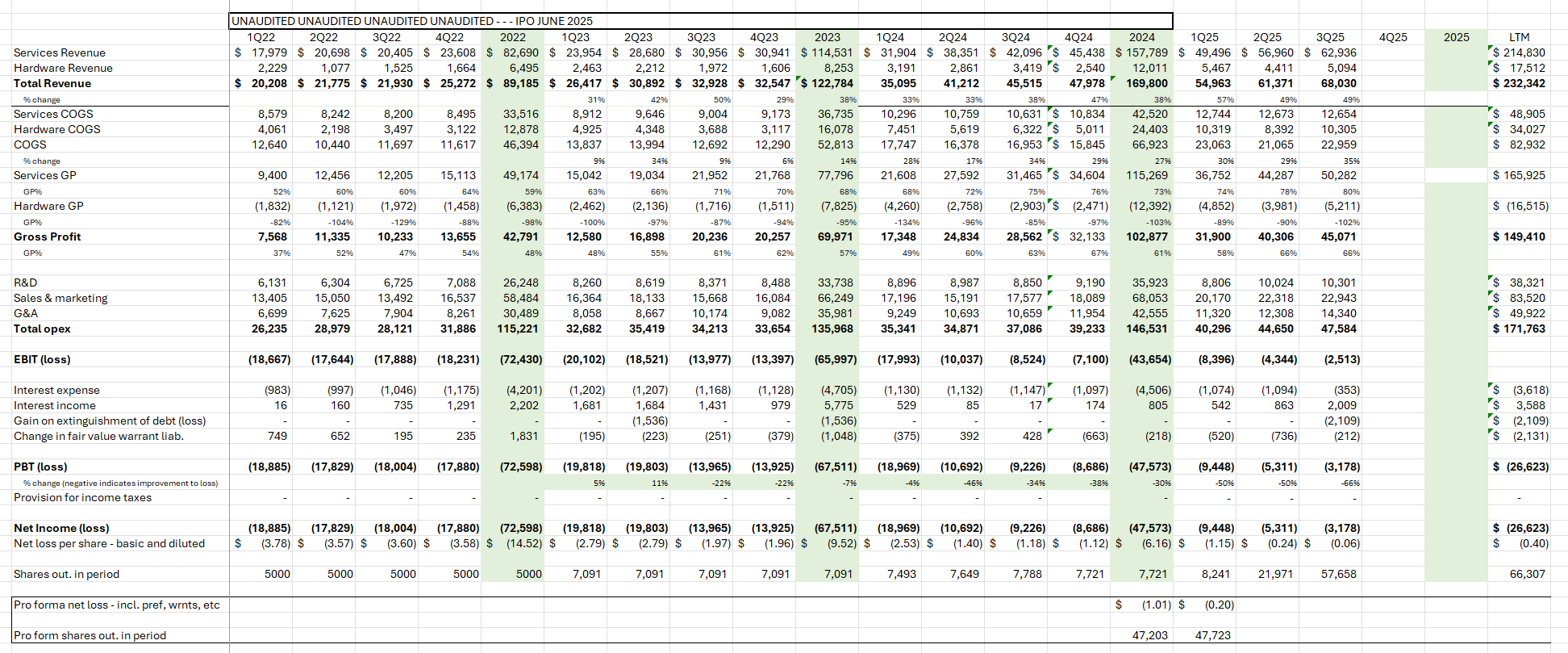

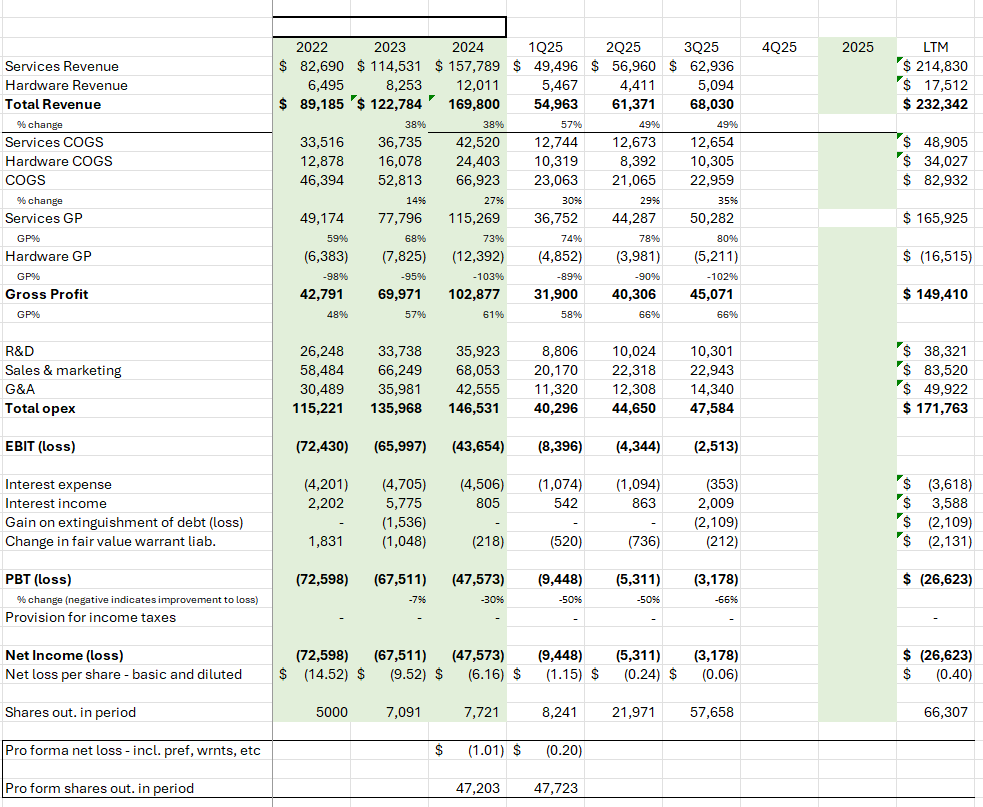

Prior to getting too deep into modeling potential growth, I gathered their historical results. Those results were unaudited, but filed in their S1. On a margin basis, I actually do like this business, but I want another quarter or two of being a public company to decide before I take a position.

The services business is what you would actually engage with, that’s Omada’s actually work product that guides people through each of their programs and helps reduce medical spend at the plan level. The hardware business is some of the materials I mentioned previously – smart scales, glucose monitors, etc.

The business has a nice gross margin profile. Consolidated gross margins are growing, from 48% to 61% 2023-2025. In 2025, that margin continued. They’ve had great top line growth and are definitely inflecting to be profitable in 2026. Their LTM PBT is a loss of $26 million, in FY24 they had a $47 million PBT loss. In their preliminary results for Q4 they highlighted 50% top line growth. They are definitely growing and my guess in FY 2026 it’s possible they become profitable.

The inflection is key to me, it’s clearly there and with the growth in Q4 to topline, barring any excess costs incurred by the company, it will feed into EBIT and PBT.

Conclusion

Their model seems to work. They have the tailwind of increased appetite for GLP-1 assistance from the membership as well as strong integration within a major managed care organization. I have concerns about the accounts receivable, however. It may be me nitpicking, but with a recent IPO like this I think it’s prudent to wait.

It’s tough to generate ideas often, if you’re finding “great investments” constantly, you’re probably not doing that good of a job actually analyzing those companies. At least that’s my view. I thought it would be helpful to share how I go about thinking of these types of companies and why I may or may choose to pass on taking a position. I used to get frustrated that I would do work on a specific stock only to end up passing on it, now it doesn’t bother me. You learn something each time and you can act when it becomes too “cheap” to pass up, if that ever occurs.

As always, DMs open, @KarstResearch on X.